Private Lending And Alternative Financing: An Introduction To Non-Bank Funding Options

Cost factors and pricing considerations for non-bank financing in the United States

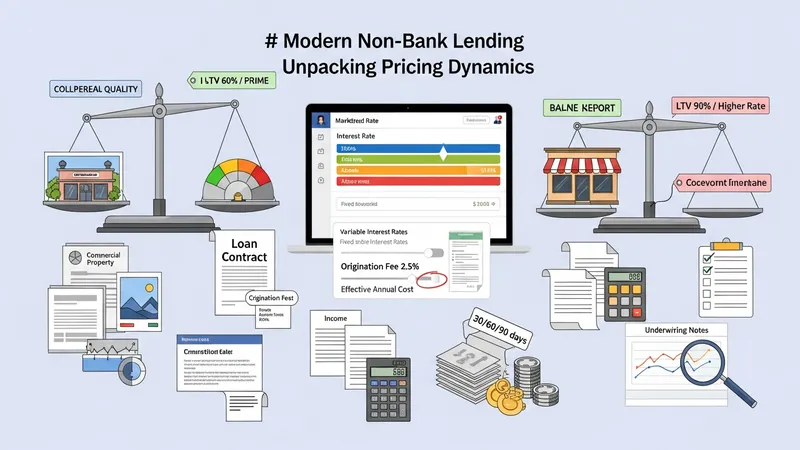

Pricing in non-bank financing typically reflects a combination of interest rate, origination or platform fees, servicing charges, and any points charged at closing. Interest components can be fixed or variable and are often influenced by borrower credit profile, collateral value, loan term, and current market rates. Origination fees or underwriting charges are common on marketplace and private deals and may be expressed as a percentage of principal. Effective annual cost calculations that include fees and amortization patterns may provide a clearer comparison across offers than headline rates alone.

Loan-to-value (LTV) and collateral quality materially influence pricing for asset-backed financing. For secured commercial or real estate financing, lower LTVs and high-quality collateral typically correspond to more favorable pricing patterns, whereas higher LTVs can produce higher quoted rates or additional covenant requirements. For unsecured consumer or small-business financing on marketplace platforms, credit scores, income documentation, and debt-to-income ratios often drive rate tiers. Specialty finance products such as invoice financing price primarily on receivables aging and customer creditworthiness.

State regulatory frameworks and disclosure obligations can affect effective cost. Some states impose licensing or rate-related restrictions that shape fee structures for particular loan types. Federal rules administered by the Consumer Financial Protection Bureau may require standardized disclosures under Truth in Lending Act or other statutes depending on product classification and lender type. Borrowers and lenders often review all applicable fees, prepayment penalties, and default remedies to understand true financing costs over the expected term.

Market comparability requires attention to term length and amortization. Short-term bridge financing often features different fee profiles and higher periodic rates compared with longer-term amortizing loans. Some marketplace-originated loans may be packaged for investor sale, altering servicing fees and secondary-market spreads. For commercial borrowers, structuring may include interest-only periods, balloon payments, or warrants that affect long-term cost. Careful modeling of expected cash flows against proposed payment schedules can clarify which financing arrangements align with an entity’s obligations and project economics.