Modular Home Financing: Steps To Prepare Your Budget And Application

Loan Types, Typical Terms, and Qualification Factors Relevant to Factory-Built Units

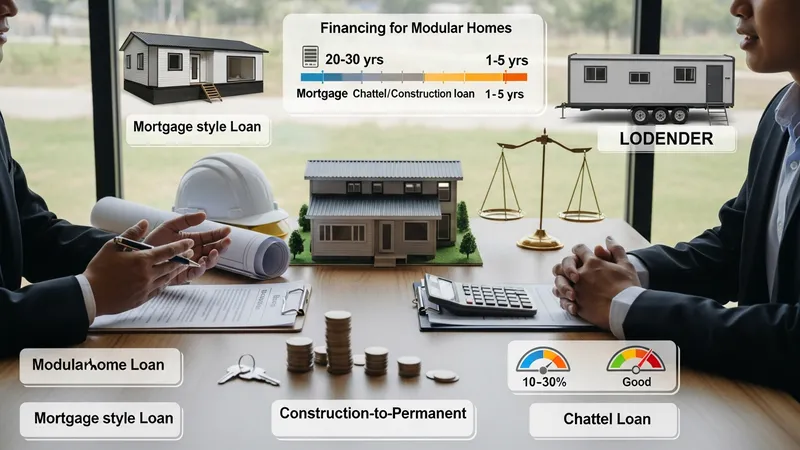

Financing approaches for factory-built units commonly include mortgage-style loans secured by the completed real property, construction-to-permanent loans that convert once the structure is installed, and personal property or chattel loans when the unit is not permanently affixed. Each approach may involve different underwriting standards, repayment terms, and collateral considerations. Term lengths for long-term financing often range from two decades to three decades where mortgage structures are used, while chattel or construction-only products frequently have shorter initial terms. Understanding the broad categories helps frame which documentation and timelines lenders will require.

Down payment expectations often vary by loan type and borrower profile; lenders may request higher initial payments where perceived project risk is greater. Typical down payment ranges are sometimes cited in percentage terms and may be influenced by credit position, loan-to-value calculations specific to the combined land-plus-unit value, and whether the borrower has substantial reserves. Interest rate levels and terms are sensitive to market conditions and borrower credit attributes; these influences are non-deterministic and change over time. Lenders may also include borrower escrow requirements for taxes and insurance where relevant.

Lender underwriting frequently considers the relationship between documented project costs and appraised value upon completion. Appraisals for factory-built units may involve comparative analysis of similar constructed properties or replacement-cost approaches depending on local appraisal practices. Where appraised value differs materially from the combined contract price and site improvements, lenders may request additional documentation, adjustments to loan sizing, or increased borrower equity. Clear, itemized contracts that tie unit specifications and installation responsibilities to firm prices can assist the appraisal and underwriting review.

Qualification can also hinge on coordination among multiple parties: manufacturer, local contractor for site work, and the lending institution. Lenders often review manufacturer warranties, production timelines, and contractor qualifications as part of assessing project completion risk. Where funds are released in stages, lenders may require inspection reports or lien releases at each disbursement point. Applicants commonly benefit from documenting the sequence of responsibilities and agreed inspection triggers to explain how funds will be applied and how project milestones will be validated by independent parties.