Cloud Billing Management: Key Features, Modules, And Workflow Overview

Compliance and taxation considerations in France for Cloud Billing Management: Key Features, Modules, and Workflow Overview

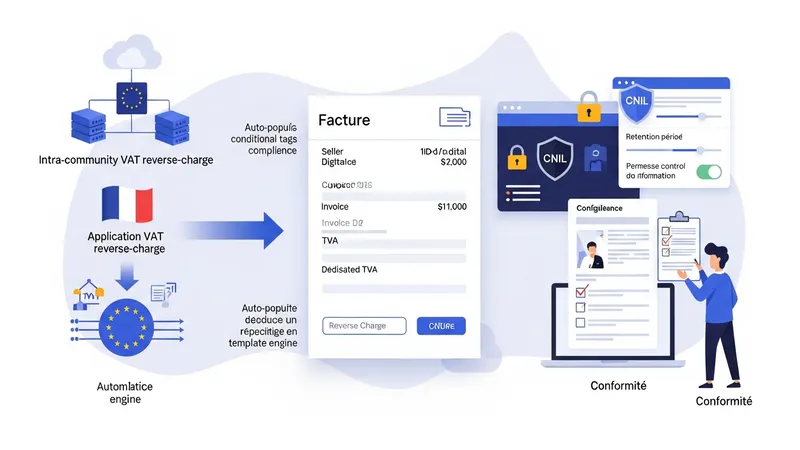

Tax and invoice compliance influence several billing design decisions. French invoicing rules, as summarized on service-public.fr, specify certain invoice elements such as seller and buyer identification, invoice date, and TVA details when applicable. Billing platforms typically include template engines that populate these fields automatically. Organisations operating across EU borders may also need to account for intra-community VAT rules and apply reverse-charge mechanisms where appropriate, which billing logic must represent as conditional tax entries on invoices.

Data protection and localisation may affect how usage records are stored and processed. The CNIL (cnil.fr) provides guidance on personal data handling that can apply when usage records include personal identifiers or when invoices contain customer personal data. French organisations often document data flows and retention periods in order to demonstrate compliance; billing systems may offer configurable retention policies and access controls to meet such requirements.

Auditability is an important compliance dimension. Billing systems in France often retain historical versions of invoices, rating configurations, and raw usage records to support financial audits and tax inspections. Secure logging, non-repudiation of invoice issuance, and exportable audit trails are typical features that finance teams request. Maintaining a clear mapping between rated usage and produced invoices helps address questions in tax reviews or internal accounting validation.

Local statutory reporting and corporate accounting standards can shape invoice formats and export standards. Many French companies integrate billing outputs with local accounting software and follow chart of accounts conventions used in France. Providing structured exports (e.g., CSV or XML with localization) and aligning invoice numbering and dating policies to French commercial code practices are considerations that may simplify downstream accounting and fiscal reporting.