Cash-Out Refinance Calculator: Estimating Potential Loan Amounts And Equity Access

Interest Rate, Costs, and Repayment Assumptions in Cash-Out Modeling

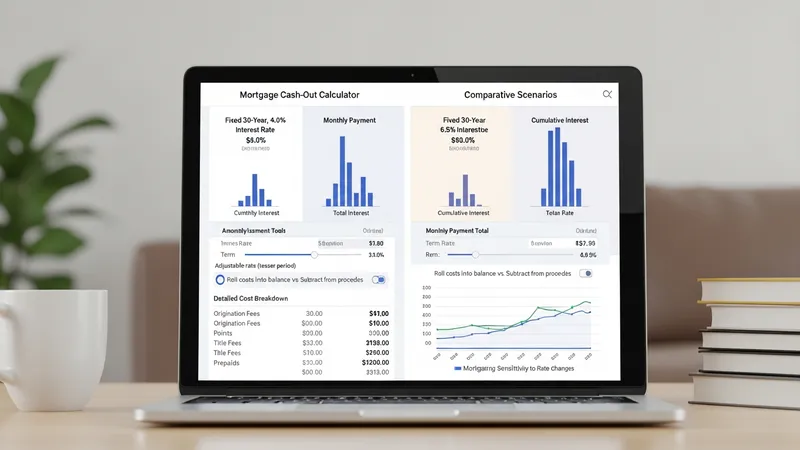

Interest rate assumptions significantly affect modeled monthly payments and long-term interest totals. Calculators commonly let users specify a rate and loan term to produce an amortization schedule or monthly payment estimate. Choosing a longer term typically reduces the modeled monthly payment but increases cumulative interest in the scenario. Some tools also offer adjustable-rate product options with initial teaser periods, while others only model fixed-rate structures. Because rate inputs are hypothetical, presenting a range of rates in parallel scenarios helps demonstrate the sensitivity of payment outcomes to interest-rate variation.

Upfront costs such as origination fees, points, title fees, and prepaids may be entered as explicit fields in detailed calculators or omitted in simpler models. How a tool treats these costs matters: when they are rolled into the new loan balance, modeled proceeds and payment will differ from a calculation that subtracts costs from proceeds. Additionally, estimated mortgage insurance premiums or escrow reserves may be shown as separate line items impacting monthly obligation estimates. Transparent tools that list included cost categories reduce the risk of misinterpreting net proceeds and payment projections.

Amortization assumptions—such as whether the modeled loan uses standard principal-and-interest amortization or interest-only periods—change the characterization of cash flow and accrued interest in a scenario. Interest-only models will present lower early payments but higher payments later when principal amortization begins, and total interest modeled over the loan term is typically higher. Calculators that permit alternate amortization schedules enable users to compare how repayment structure interacts with chosen term and rate inputs within the same scenario framework.

Transaction timing and one-time charges are additional considerations. Prepayment penalties on existing loans, rate-lock fees, or seller credits may be relevant in real transactions but are not uniformly represented in calculators. Clear labeling of which transaction costs are included—and whether the model assumes costs are financed into the new loan or paid out of proceeds—helps readers interpret results. These distinctions are important when comparing modeled scenarios or preparing for formal lender discussions.