Cash-Out Refinance Calculator: Estimating Potential Loan Amounts And Equity Access

How Equity and Loan-to-Value Calculations Determine Estimated Proceeds

Available equity in a modeled scenario is generally derived by subtracting outstanding lien balances from the chosen property value input. A calculator then applies an allowable LTV percentage to the property value to determine a maximum new loan amount. The modeled proceeds equal the maximum new loan minus the sum of existing payoff amounts and selected closing costs when the tool includes those deductions. This structure means that both the assumed property value and the specified LTV cap directly constrain the projected proceeds; changes to either input often have a larger proportional effect on proceeds than small interest-rate adjustments.

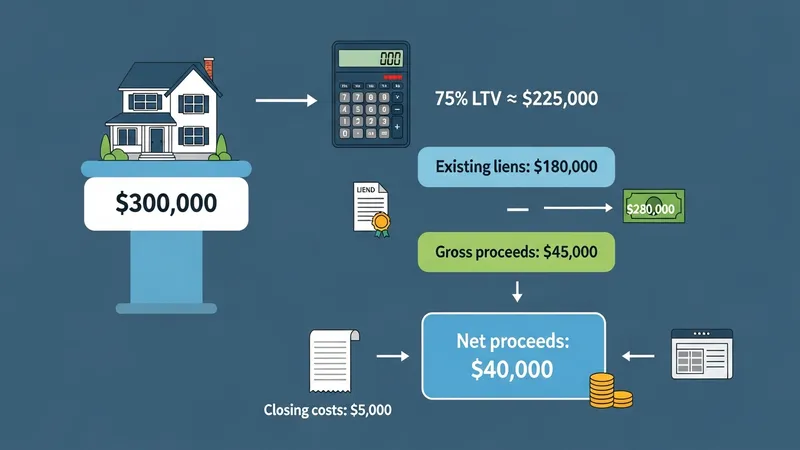

Examples help illustrate typical mechanics without implying specific product terms. If a modeled property value is 300,000 and existing liens total 180,000, the nominal equity is 120,000. Applying an LTV cap of 75% yields a maximum new loan of 225,000, and subtracting the 180,000 payoff suggests gross proceeds of 45,000 before costs. If estimated closing costs are included and equal 5,000, a calculator that deducts costs would show net proceeds of 40,000. That simplified example demonstrates how value, LTV, and cost treatment combine in most estimate tools.

Multiple liens and second mortgages introduce additional complexity that many calculators account for in one of two ways: by listing each existing lien as a payoff item to subtract from the new loan, or by allowing a combined outstanding balance entry. Accurate input of subordinate lien balances is important where present because those payoffs reduce modeled net proceeds. Some calculators also permit modeling of a new loan that pays off both first and second mortgages; in such cases, the new loan must still satisfy the LTV constraint based on the selected property value input and policy limit.

Sensitivity testing across realistic ranges of value and LTV can reveal constraints and trade-offs. Increasing the modeled property value raises both the maximum loan at a fixed LTV and the projected proceeds, while increasing the LTV cap boosts the allowable loan amount but raises leverage on the property in the scenario. Because these are modeling parameters rather than underwriting guarantees, users often run several permutations to understand how robust their goals are to differing valuation or policy assumptions.