Carbon Accounting Software: How Enterprises Track Emissions And Environmental Impact

Carbon Accounting Software: Emissions Calculation Methods and Scopes

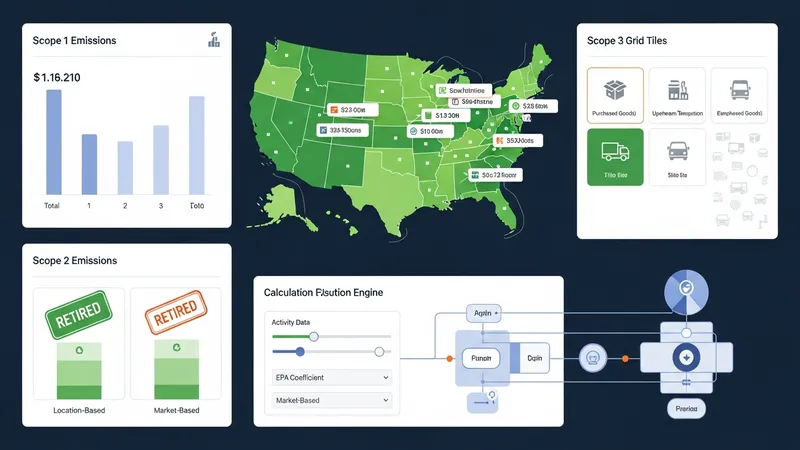

Emissions calculation methods implemented in software generally reflect established protocols and region-specific emission factors. In the United States, tools often include factors for electricity grid mixes, state-level fuel factors, and EPA-recommended coefficients. Calculation modules typically allow users to select the appropriate scope classifications—scope 1 for direct emissions from owned sources, scope 2 for purchased energy, and scope 3 for indirect value-chain emissions. Software may provide configurable calculation engines to apply activity data to emission factors and aggregate results by facility, business unit, or product line.

Scope 2 accounting commonly uses location-based and market-based methods; many US organizations track both to reflect physical grid emissions and contractual instruments such as renewable energy certificates (RECs). Software may support dual reporting and maintain documentation of supplier contracts or certificate retirements. Scope 3 categories—such as purchased goods, upstream transportation, and employee commuting—may require proxy methods or spend-based approaches when direct activity data are unavailable, and software often includes templates or default factors to facilitate preliminary estimates.

Software that supports scenario analysis and emission intensity metrics can aid internal decision-making. Enterprises in the United States sometimes calculate emissions per unit of production, per revenue dollar, or per full-time employee to compare performance across divisions. Calculation transparency—exposing the emission factors used, conversion steps, and any applied assumptions—is commonly important for internal review and external assurance. Platforms frequently provide exportable worksheets that document calculation logic for auditors.

Uncertainty management is another calculation-related consideration. Many tools allow users to annotate data with confidence levels or to run sensitivity analyses to show how changes in activity data or emission factors affect totals. For US enterprises that participate in voluntary reporting or that anticipate regulatory oversight, maintaining records of assumptions, data sources, and uncertainty estimates may support more robust disclosure and facilitate third-party validation.