SUV Financing: Understanding Loan Terms, Interest Rates, And Fees

Interest rate types, APR disclosure, and calculation considerations

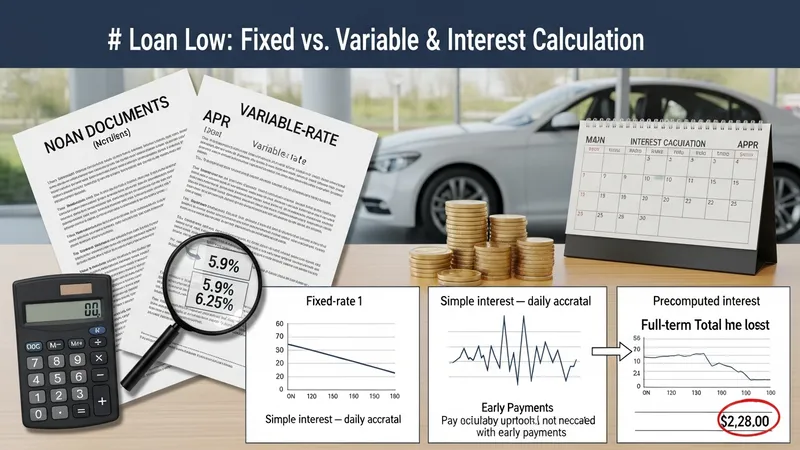

Interest rates on vehicle loans can be presented as a nominal rate or as an annual percentage rate (APR) that attempts to capture periodic interest plus certain fees. Fixed-rate loans maintain the same nominal rate over the contractual period, producing predictable periodic interest amounts. Variable-rate loans tie the rate to an index plus a margin and can change over time, which may result in fluctuating periodic interest or adjustments to the repayment schedule. When comparing offers, examining both the quoted nominal rate and the APR may provide a broader sense of comparative cost.

Calculation conventions determine how interest accrues and is applied to the outstanding balance. Simple interest loans compute interest daily on the outstanding principal and apply it to monthly payments; this method typically results in lower interest if extra payments are made. Other arrangements may use precomputed interest where interest for the full term is calculated upfront, which can affect the benefit of early repayment. Clarifying the interest computation method in contract documents is an important step for understanding how payment timing influences total interest paid.

Credit profile and market conditions commonly influence the interest rate offered. Lenders assess credit history, debt-to-income measures, and sometimes the vehicle’s age or warranty status when setting a rate. Broader market interest rate environments also affect pricing and product availability. Quoted rate ranges may therefore vary noticeably between applicants and over time. A cautious approach is to view rate quotes as conditional snapshots that may change with underwriting outcomes or shifts in financial markets.

APR disclosures and itemized cost summaries are designed to facilitate comparison, though exact inclusions can differ by jurisdiction and lender practice. Some fees, such as certain administrative charges, may be included in APR calculations while others are excluded, which can complicate direct comparison if not reviewed carefully. Requesting an itemized cost summary or sample payment schedule helps to reconcile differences in advertised rates and to assess the effective carrying cost of the loan under different payment scenarios.