Small Business Liability Insurance: Key Coverages And What They May Protect

Policy Structures, Limits, and Deductibles Relevant to U.S. Small Firms

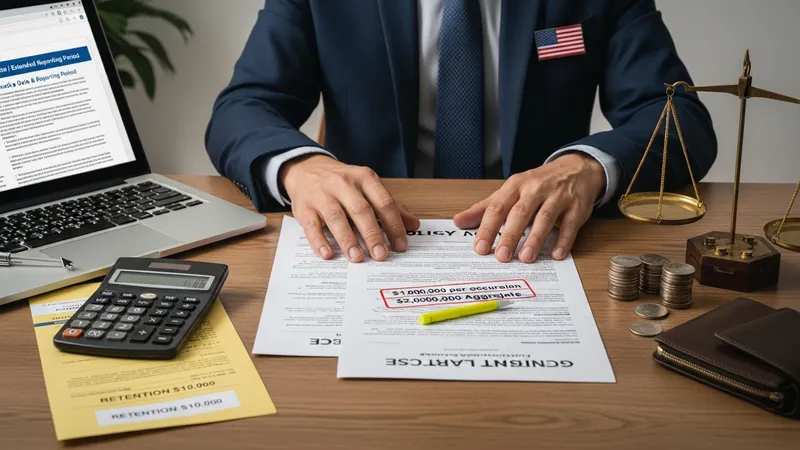

Insurance contracts for liability exposures usually specify per-occurrence limits and aggregate limits for the policy term; these terms determine the maximum insurer obligation for a single event and for all events combined. Many U.S. small businesses commonly see illustrative limit structures such as $1,000,000 per occurrence with a $2,000,000 aggregate, though actual choices vary by industry, contract needs, and insurer underwriting. Deductibles or retentions can lower premium costs but increase out-of-pocket expenditure when a claim arises. It is common practice to balance limit selection against the financial capacity to absorb retained amounts.

The distinction between occurrence-form and claims-made policies is significant, especially for professional and cyber liability lines. An occurrence policy may respond to an event that occurs during the policy period even if the claim is made later, whereas a claims-made form typically requires the claim to be reported during the policy period (or an extended reporting period) for coverage to apply. Small firms in the U.S. that change insurers or purchase retroactive coverage often review these differences carefully because they affect long-term exposure handling and continuity of protection.

Umbrella and excess liability policies add broader or higher limits above underlying primary policies. An excess policy typically provides additional limits once the underlying policy limits are exhausted, while an umbrella policy may also contain coverage language that fills certain gaps. In the U.S., contractual requirements—such as lease agreements or client contracts—may stipulate minimum underlying limits before an umbrella can attach. Businesses should recognize that umbrella layers depend on the presence and scope of primary policies to function as intended.

Endorsements and policy form variations can materially change the effective coverage scope. Common endorsements in U.S. liability policies include additional insured status for contractual partners, waiver of subrogation, and specialized exclusions or extensions for specific operations. These modifications may be included to satisfy contract conditions or to tailor protection to particular exposures. When available, insurers or neutral industry resources can explain how typical endorsements alter policy behavior over time.