Private Lending For Property: Key Features, Loan Structures, And Typical Uses

Private Lending for Property: Loan Structures and Key Terms

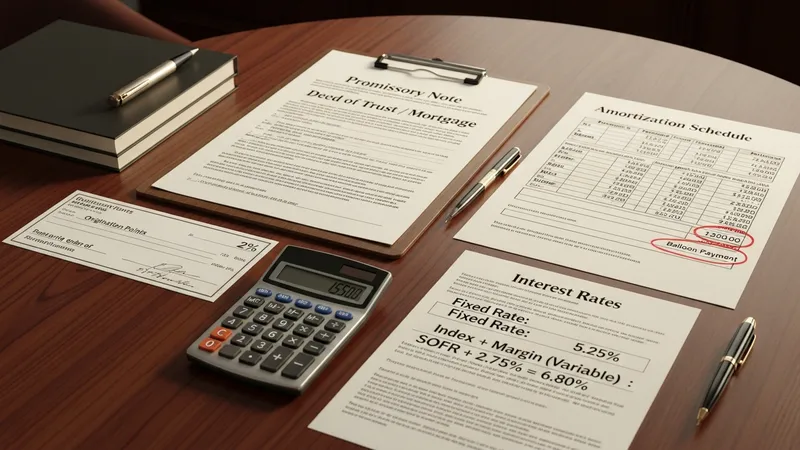

Private property loans use a variety of legal and financial instruments that define the lending relationship. Common instruments include a promissory note setting payment obligations and either a deed of trust or mortgage creating the lien on the property. In many U.S. states a deed of trust is the preferred security instrument; in others a mortgage is used. Loan covenants may specify interest calculation (simple or compound), payment frequency, default remedies, and whether the loan is non-recourse or recourse. Balloon payments, amortization schedules, and prepayment conditions are typically negotiated to match the borrower’s planned exit strategy.

Interest rate formats in private lending can be fixed for the loan term or variable based on an index plus a margin, although fixed short-term rates are common for projects with predictable payoffs. Lenders often charge origination points (a percentage of principal paid at closing) and may add closing costs such as appraisal, title, and recording fees. Amortization periods, when used, may be longer than the actual loan term, creating a final balloon payment that requires refinancing or sale. These structural choices affect borrower cash flow and lender return expectations.

Loan-to-value and loan sizing practices are central to structure. Private lenders typically set LTV limits that reflect the property’s condition, use, and market liquidity; for renovation loans this may be framed against after-repair value (ARV). Credit underwriting may place more emphasis on collateral value and exit feasibility than on conventional credit scores, although borrower experience and track record often reduce perceived risk. Reserves or contingency holdbacks are sometimes included to cover rehabilitation overruns or delayed project timelines.

Security and enforcement provisions also shape loan terms. Private loan agreements often include cross-default clauses, guaranties, and specific performance remedies. In the United States, foreclosure remedies and timelines vary by state; lenders commonly factor local foreclosure process duration into term and pricing decisions. Title insurance, environmental reviews, and survey requirements are frequently part of closing to verify collateral status and reduce post-closing legal exposure.