Private Business Loans: How Small Businesses Can Access Alternative Financing

Underwriting, documentation, and operational considerations for private business loans

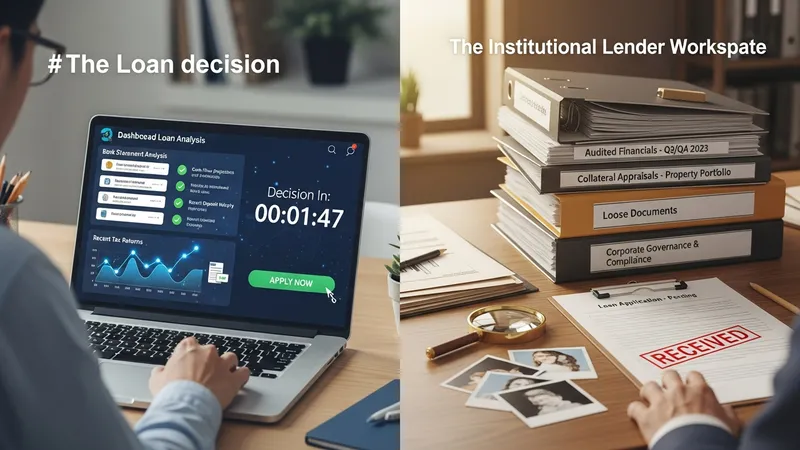

Underwriting standards for private business loans in the United States typically focus on recent cash flow, bank deposits, and business performance metrics, though requirements vary by lender type. Online lenders frequently request several months of bank statements, recent tax returns, and owner personal credit checks. Invoice financiers require proof of invoices and customer payment histories. Private credit funds may request audited financial statements, corporate governance details, and collateral appraisals for larger commitments.

Documentation timelines and processes differ: online platforms often automate verification and can issue decisions in days, while institutional lenders may take weeks to complete credit approval. Operationally, borrowers should anticipate reconciliation tasks tied to receivable-based financing, such as remitting collections or providing ongoing reporting. Maintaining organized financial records and bank statement histories can improve speed and reduce friction during underwriting, especially for lenders that rely on automated data analysis.

Repayment mechanisms also present operational effects. Daily or percentage-of-sales remittances require compatible point-of-sale and cash management systems so repayment flows do not disrupt payroll or vendor payments. For invoice-based advances, companies often need to manage collections protocols in coordination with their financing partner. Awareness of these operational implications helps firms assess operational fit alongside cost and availability when evaluating private loan options.

Credit documentation often contains covenants, default definitions, and events of acceleration that differ from bank loan agreements. Small businesses in the United States may find it useful to have a legal review of term sheets and borrower obligations to understand reporting triggers or restrictions on additional indebtedness. Framing these contractual terms as considerations rather than directives helps clarify how lender requirements may affect future financial or operational flexibility.