Private Business Loans: How Small Businesses Can Access Alternative Financing

Types of private financing options for small businesses in the United States

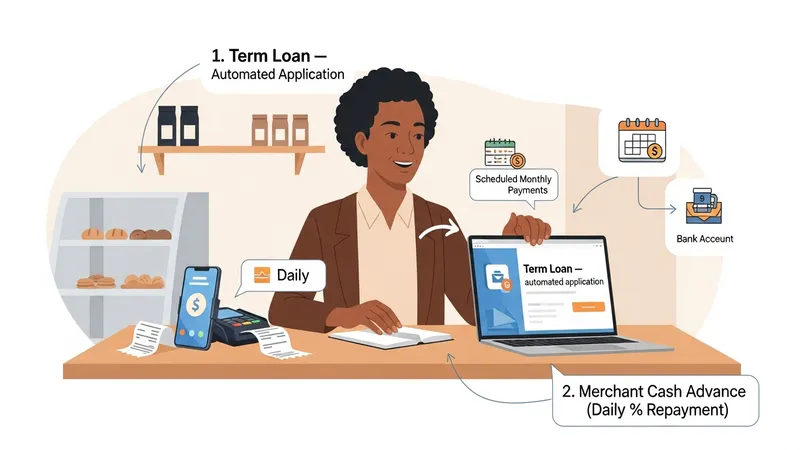

Private financing in the U.S. takes several distinct forms that small businesses may consider depending on needs. Online term loans provide lump-sum financing repaid over a set period and often use automated applications; examples include lenders like OnDeck. Revolving lines of credit, such as those offered by BlueVine, allow drawdowns up to an approved limit. Invoice financing or factoring (e.g., Fundbox) converts receivables into working capital and may be structured as an advance against outstanding invoices.

Merchant cash advance (MCA) providers offer advances repaid via a portion of daily credit-card sales or fixed daily withdrawals; these arrangements often have different fee structures than term loans. Private credit funds and institutional mezzanine lenders may provide larger facilities or equipment financing, usually with more extensive documentation and longer negotiation timelines. Each type aligns with different cash-flow patterns: MCAs link to daily sales, invoice financing to receivables, and term loans to scheduled repayments.

Market usage patterns in the United States suggest these forms coexist because of varied borrower profiles. The Federal Reserve’s Small Business Credit Survey and related industry reports often note that smaller, newer firms use online platforms more frequently for quick access, while established companies may access private credit funds for sizable, structured financing. This segmentation reflects how underwriting criteria and product features typically map to business lifecycle and financing scale.

When comparing categories, consider scalability and administrative cost. Invoice financing can scale with receivables but may require ongoing verification of invoices; lines of credit offer flexibility but might have maintenance fees or variable rates. Private credit fund transactions may include covenants or reporting obligations that affect operations. These differences are typical considerations rather than prescriptions, and they may affect which product matches a firm’s financial profile and operational needs.