Mortgage Refinance And Home Loan Rates: Key Factors That Influence Borrowing Costs

Loan structure choices: fixed-rate versus adjustable-rate and term length impacts

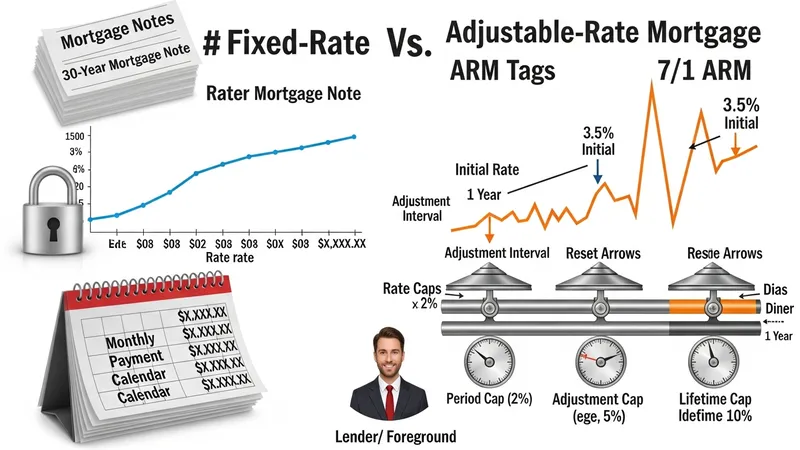

Loan structure choices directly influence how a borrower experiences interest rate risk and payment variability. Fixed-rate loans maintain a constant nominal rate for the agreed term, which can provide predictable monthly payments; adjustable-rate mortgages (ARMs) typically begin with a stated initial rate and then reset periodically based on a referenced index plus a margin. In the United States, conventional mortgage terms often include 15- and 30-year fixed options and various ARM structures such as 5/1 or 7/1 ARMs, where the first number indicates the fixed initial period and the second the annual adjustment frequency thereafter.

ARMs can feature rate caps, adjustment ceilings, and lifetime caps that limit how much the rate can change at a single adjustment or over the life of the loan. Lenders and investors price ARMs by accounting for expected future index movements and borrower risk factors; as a consequence, initial ARM rates may be lower than comparable fixed-rate offers but carry adjustment risk. Fixed-rate pricing typically reflects longer-term rate expectations and investor demand for stable cash flows, which can lead to different spreads over benchmark yields compared with ARMs.

Term length affects both the monthly payment and the long-term interest paid. Shorter terms generally result in higher monthly payments but lower total interest over the life of the loan, while longer terms reduce monthly payments but may increase total interest. In the United States, consumer preferences, income stability, and plans for home tenure all interact with term choice; lenders may present amortization schedules to illustrate how principal and interest allocation change over time for different term options without implying one choice is universally preferable.

Lender pricing models incorporate structural elements as part of their risk assessment; for example, loans with less common term lengths or features may be harder to sell in the secondary market and thus carry pricing adjustments. Mortgage-backed securities markets and program eligibility influence which loan structures are most commonly offered at competitive spreads. Observers often compare scenario illustrations for fixed and adjustable options to estimate payment trajectories under varying rate conditions rather than to predict a single outcome.