Mortgage & Real Estate Financing: Key Loan Types And How They Work

Interest Rate Types and Mechanics related to Mortgage & Real Estate Financing: Key Loan Types and How They Work

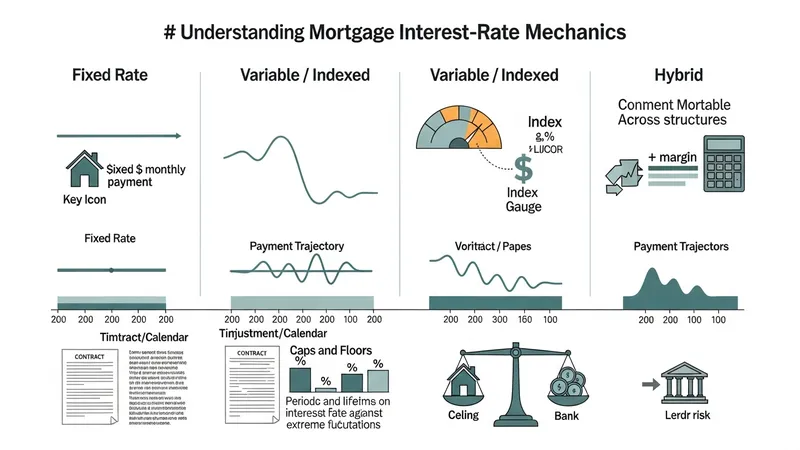

Interest-rate design is central to loan behavior; common categories include fixed, variable/indexed, and hybrid models. Fixed rates give payment predictability for the contract period, while variable rates tie to an index plus a margin, creating exposure to market movements. Hybrid models may offer a fixed initial period followed by a variable phase. Rate adjustments are often governed by specified indexes, adjustment intervals, and caps that limit the magnitude of changes in a period or over the loan life.

Variable-rate loans require clarity on the referenced index and margin because those components determine future payment adjustments. Index choices may be short-term money-market rates or published benchmark rates. The margin is a fixed amount added to the index to form the effective rate. Caps and floors may be included to prevent extreme movement; periodic caps limit change at any reset, while lifetime caps limit total change across the term. These features aim to balance borrower affordability with lender risk management.

Fixed-rate loans protect borrowers from rising rates but transfer rate risk to the lender; consequently, lenders often price fixed products to reflect anticipated rate movements and funding costs. Prepayment clauses are frequently associated with fixed-rate loans to manage the lender’s exposure to early repayment when market rates fall. In markets where refinances are common, the interplay between fixed-rate pricing and prepayment provisions can materially affect borrower decisions over time.

From a risk-management perspective, lenders and secondary-market participants may hedge interest-rate exposure using financial derivatives or funding strategies. These practices influence product availability and pricing. For borrowers, understanding how rate design impacts monthly obligations and total interest is important when selecting between fixed, variable, or hybrid structures, particularly when considering expected holding periods and cash-flow tolerances.