Home Equity Line Of Credit: How HELOCs Work And Key Features To Understand

Credit limits and equity calculations for home-secured revolving credit

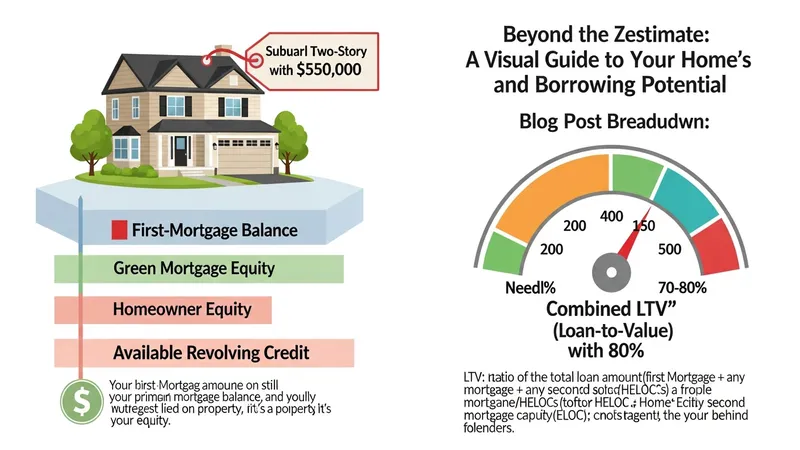

Credit limits for these arrangements are typically determined by combining the existing mortgage balance with a lender-set maximum loan-to-value ratio and comparing that sum to the property valuation. The process may use a professional appraisal, an automated valuation model, or a broker-supplied estimate. Lenders often express limits as a percentage of the home’s assessed market value, and underwriting can include factors such as borrower credit history and debt-to-income ratios. These criteria may vary significantly among providers and over time as market conditions change, so approved limits can differ even for similar properties.

Combined LTV calculations usually consider all secured liens on the property. For example, a higher outstanding first mortgage reduces the remaining equity available for a revolving credit line, while a lower outstanding balance increases potential availability. Seasoning rules—how long a borrower has owned the property—may also influence eligibility. Some lenders set internal thresholds for maximum combined LTV that reflect their risk tolerances; these thresholds can alter the portion of assessed value that may be accessible through this type of credit.

Valuation method choice can materially affect the calculated limit. Appraisals that identify recent local sales and property condition may produce different values than algorithmic models relying on public data. Lenders may require additional documentation if the valuation method yields uncertainty, and this can affect the timeline and final approved limit. Borrowers often see variability in limits across lenders because of differences in how conservatively each party estimates value and adjusts for factors like property type or market volatility.

Insider considerations include anticipating how planned property improvements or changes in the mortgage balance could alter available credit over time. For households expecting to reduce a primary mortgage balance or to complete qualifying improvements, the available limit may increase. Conversely, market declines in valuation or increases in secured debt can reduce available credit. Understanding these dynamics can help set realistic expectations about potential access to funds across the life of the arrangement and inform comparisons among product features.