Financial Technology Trends: Key Innovations Reshaping Banking And Payments

Platform types and feature coverage in banking and payments

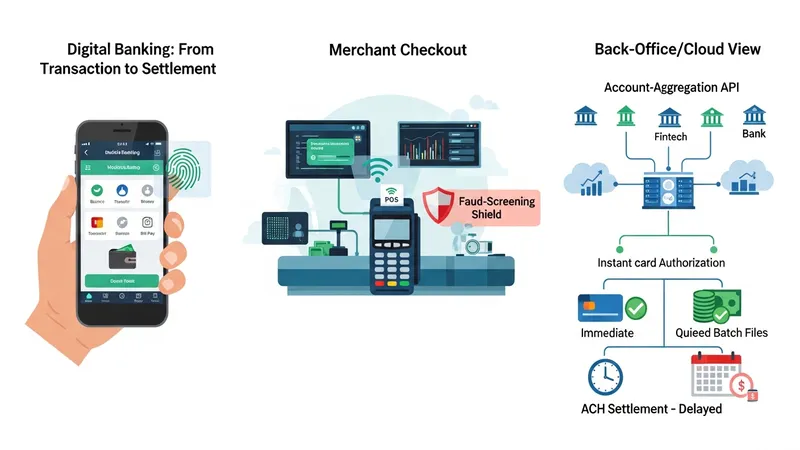

Platform selection in U.S. banking and payments often falls into categories such as consumer mobile banking apps, merchant payment gateways, account-aggregation APIs, and back-office clearing systems. Consumer apps typically provide balance viewing, transfers, and bill payment features and may integrate with mobile wallets like the previously listed services. Merchant gateways focus on payment authorization, fraud screening, and payout capabilities. Account-aggregation APIs enable third-party apps to securely query balances and transactions, which many U.S. fintechs and banks use for underwriting or cash-flow tools.

Feature coverage can be examined across authentication, settlement timing, dispute management, and reporting. For example, device-based authentication combined with multi-factor authentication may be used to reduce fraud risk, while settlement timing differences between card networks and automated clearinghouse (ACH) rails affect cash flow. U.S. institutions often balance real-time authorization experience with batch settlement processes that are more cost-efficient for low-value transfers, and those trade-offs shape product design and user expectations.

When integrating platforms, institutions may evaluate API documentation quality, uptime guarantees, and data models. In practical terms, many U.S. banks may pilot connectivity with providers such as Plaid for account verification and Stripe or other processors for card acceptance, conducting load and failure-mode testing to understand behavior under normal and stressed volumes. These evaluations may also consider contract terms related to data use and breach notification that reflect U.S. legal frameworks.

Operational considerations in platform choice often include vendor diversity and portability of data. Institutions may prefer modular architectures that allow replacing a payment gateway or switching identity providers without reworking core account-ledger logic. Such modularity can reduce vendor lock-in risk but may increase integration overhead in the short term. These design decisions can influence ongoing maintenance costs and the ability to adopt new payment rails or regulatory requirements.