Debt Settlement And Credit Repair: Understanding Key Strategies And Potential Risks

Potential Risks, Consumer Considerations, and Long‑Term Effects

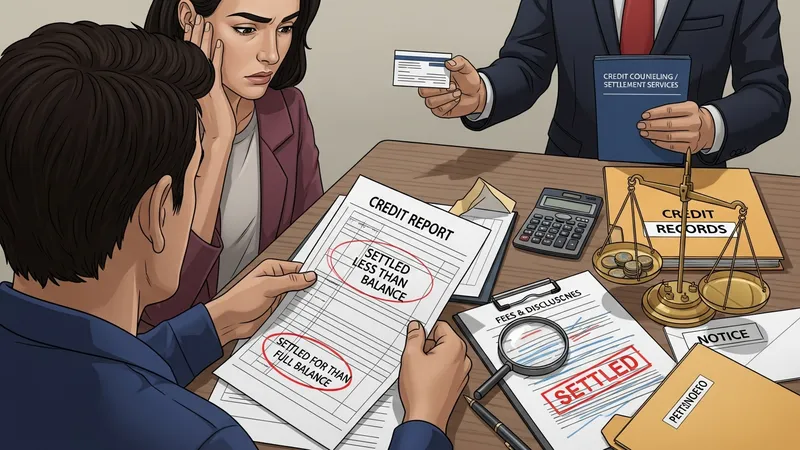

Potential risks associated with settlement and repair processes include incomplete resolution of the underlying obligation, lingering negative notations on credit records, and possible fiscal reporting effects in certain jurisdictions. Settlements that reduce principal may close an account but still leave a notation indicating a payment for less than the full balance, which many scoring models treat differently than timely payments. Dispute attempts that fail to remove accurate entries will generally leave the underlying record intact. Consequently, parties often weigh the short‑term relief of reduced balances against longer‑term record effects.

Another consideration is the role of third‑party service providers. Credit counseling, settlement companies, and repair services may offer expertise but also typically charge fees and operate under contract terms that require careful review. Industry oversight and consumer protection regulations in many jurisdictions set standards for disclosures and practices; understanding these frameworks commonly helps people evaluate the tradeoffs of using external services versus direct negotiation or self‑initiated dispute filing. Transparency in agreements and fee structures is often highlighted as important information to confirm before engagement.

Long‑term effects on creditworthiness often depend on the mix of accounts, the age of derogatory entries, and subsequent payment behavior. While settled or corrected entries may affect scoring differently, establishing consistent on‑time payments and managing credit utilization can progressively influence scoring models. Recovery timelines vary and may be influenced by the presence of public records, the number of active derogatory items, and the addition of positive account activity. Patience and ongoing monitoring are commonly cited as practical aspects of rebuilding credit standing.

Finally, documentation and follow‑up are recurring themes in guidance about reducing risk. Keeping copies of settlement letters, dispute confirmations, and updated reports can help verify that agreed changes were implemented and remain accurate. Where discrepancies appear after an agreed resolution, recorded evidence often supports clarifying discussions with furnishers or reporting agencies. These procedural safeguards are typically presented as prudent considerations rather than guarantees of specific outcomes.