Debt Settlement And Credit Repair: Understanding Key Strategies And Potential Risks

Regulatory, Reporting, and Timing Factors Affecting Outcomes

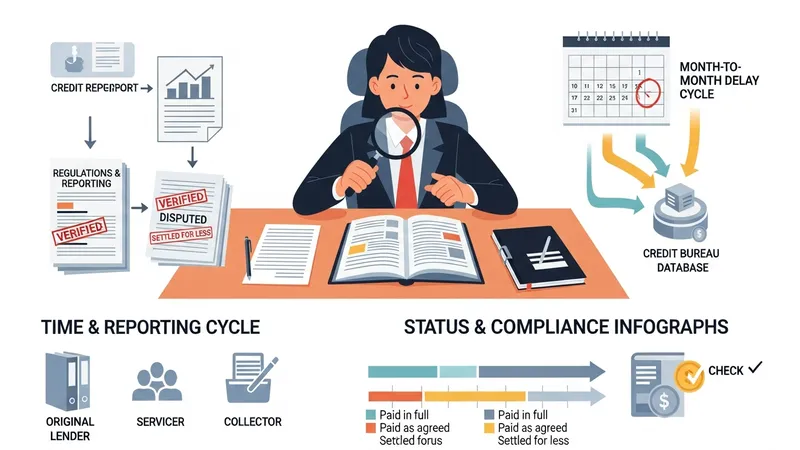

Regulatory frameworks and industry reporting practices shape how settlements and disputes are handled and how outcomes are represented on consumer records. Many systems impose deadlines for investigation responses, requirements for accuracy and completeness of reported data, and rules for how certain account statuses are categorized. Reporting cycles are frequently monthly, so changes agreed in one month may not appear on a credit file until the next reporting cycle. Stakeholders commonly consider these timing dynamics when assessing how rapidly a correction or settlement will be reflected in databases used by lenders and other decision‑makers.

Different types of data furnishers—original lenders, national or regional servicers, and third‑party collectors—may follow distinct internal policies for reporting and for responding to verification requests. This can lead to variations in how quickly an item is updated or whether a settlement is recorded as a payment in full, paid as agreed, or settled for less than full. Where disputes involve multiple furnishers or multiple reporting agencies, coordination may be required to ensure consistency. Industry guidance often highlights the need to review all three major reporting agencies or equivalent sources in a given jurisdiction.

Timing also plays a role in legal remedies and limitations. Statutes of limitation for debt collection, for example, vary by jurisdiction and by type of debt; these limitations may influence negotiation strategy and creditor behavior but do not automatically erase reporting obligations. Public records such as judgments may have separate retention periods that affect how long they appear on a report. Consumers and practitioners frequently consider both procedural deadlines and substantive limitations when evaluating potential paths and expected durations for resolution.

Practical considerations include monitoring for re‑reporting after a resolution and confirming that furnishers and reporting agencies have synchronized updates. In some cases, a corrected or settled account may be resubmitted incorrectly if internal systems are not updated, so periodic review of reports after a resolution is often advised as a verification measure rather than a directive. Understanding the cadence of reporting and the interplay of multiple data sources typically informs expectations about when improvements or changes will be visible to lenders and scoring models.