Credit Card Processing: How Payment Gateways And Merchant Accounts Work For Businesses

Payment Gateway Functions and Flow for Businesses

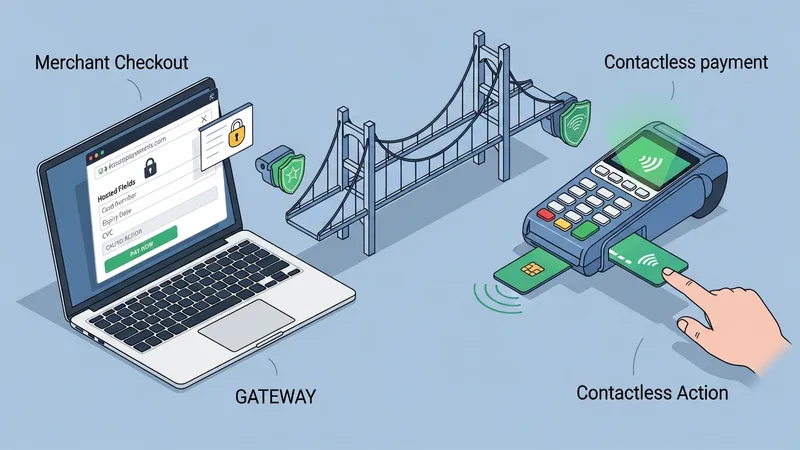

Payment gateways act as the technical bridge between a merchant’s checkout system and payment processors or acquirers. In the United States a gateway may provide hosted checkout pages, API endpoints for direct integration, tokenization services for stored credentials, and fraud screening tools. For online merchants, hosted pages and hosted fields can reduce the merchant’s handling of card data and therefore affect PCI compliance scope. For in-person commerce, gateways may also integrate with terminal hardware that supports EMV and contactless payments.

The authorization flow typically starts when a consumer submits card details: the gateway encrypts or tokenizes data, forwards it to a processor or acquirer, and receives an authorization response from the issuing bank. If approved, the merchant can capture the funds; captures may be immediate or delayed for pre-authorized transactions. Gateways commonly provide detailed transaction logs and batch reporting that reconcile authorization IDs, captures, and settled batches against the merchant’s bank statement.

Gateway selection in the U.S. often reflects integration needs and volume. API-driven gateways may suit merchants with technical resources who require custom checkout flows or subscription billing, while hosted checkout options can reduce development and compliance overhead. Many gateways also offer developer documentation, SDKs, and sandbox environments that allow merchants to test payment flows without sending live card data to networks during development.

Operational considerations include latency, uptime, and support for U.S.-centric card products. Gateways may include built-in fraud filters tuned to U.S. transaction patterns or tokenization schemes that comply with card network requirements. Merchants typically evaluate how gateways present reporting for reconciliation, whether they support multiple payment methods (card brands, wallets), and what mechanisms exist for dispute notifications and webhook events used in automated order-management workflows.