AI Finance Agents: How Intelligent Tools Support Accounting Automation

Accuracy, controls, and compliance considerations for AI finance agents

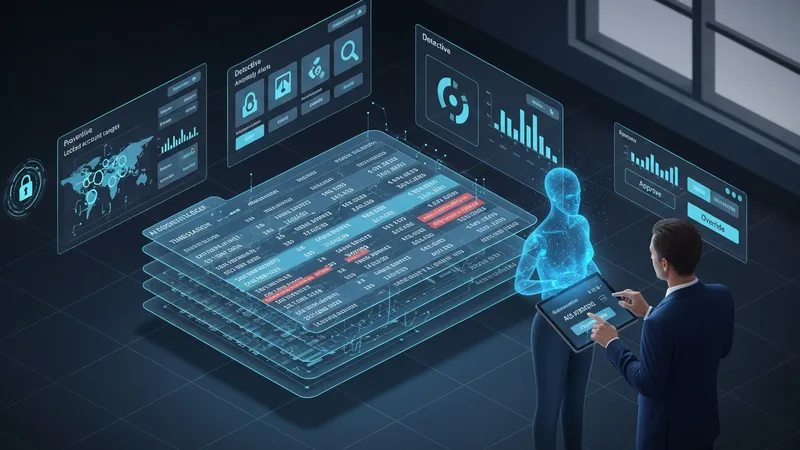

Accuracy measurement commonly uses metrics such as correct-category rate for transaction classification, field-extraction accuracy for invoices, and match rates for reconciliation. Organizations often set conservative confidence thresholds so that only high-confidence suggestions are auto-posted, while lower-confidence items are routed for human review. In the United States, public companies may evaluate how automation interacts with Sarbanes-Oxley (SOX) controls, and all entities typically consider audit trails that document who approved or changed automated outputs.

Internal controls around automated processes are usually layered: preventive controls constrain model outputs to valid account ranges, detective controls alert users to anomalies, and corrective controls document how exceptions are resolved. Vendors and internal teams often record detailed logs of automated decisions and human overrides to support auditors and inquiries from regulators such as the IRS or the Securities and Exchange Commission (SEC) where applicable. These records are typically designed to support GAAP-compliant financial reporting.

Model explainability and transparency are practical areas of focus. Finance teams may require that the system provide rationale or supporting evidence for suggested categorizations and value extractions—such as matching vendor names or prior transaction history—so reviewers can assess why a decision was made. Regular audits of model performance and periodic retraining using confirmed outcomes are commonly used to limit drift and to show that controls are operating effectively over time.

Compliance also involves retention and retrieval policies. In the U.S., standard practice is to retain records in line with IRS guidelines and to ensure that automated records are searchable for audit purposes. Contractual terms with vendors often specify responsibilities for data retention and the ability to export data if a relationship changes. These points are typical planning topics for teams considering automation and are offered as informational considerations.