AI Finance Agents: How Intelligent Tools Support Accounting Automation

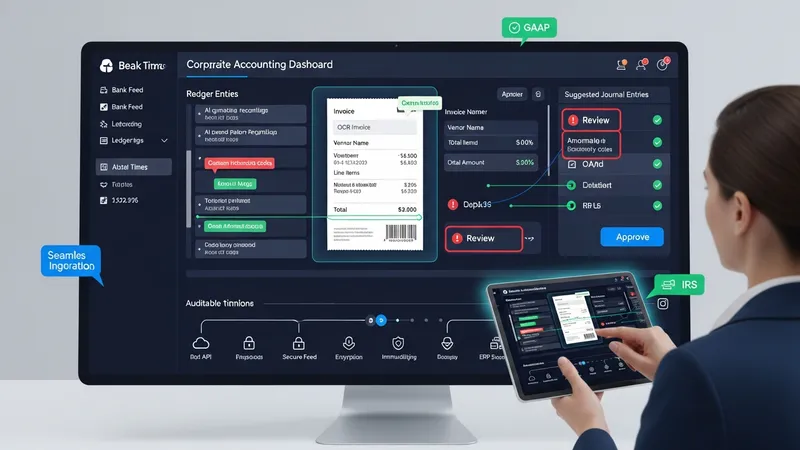

Intelligent software agents for finance automate routine accounting tasks by applying machine learning, natural language processing, and business rules to financial data. These systems ingest bank feeds, invoices, receipts, and ledger entries to perform tasks such as transaction categorization, invoice extraction, and preliminary reconciliations. Within an accounting environment, they may generate suggested journal entries, flag anomalies for review, and create structured workflows that route items to human reviewers when confidence is low. The tools typically operate alongside existing ledgers and enterprise resource planning (ERP) systems to reduce repetitive manual work and to produce auditable trails of automated actions.

Architecturally, these agents often combine optical character recognition (OCR) for document capture, pattern recognition for mapping transactions to chart-of-accounts codes, and rule-based layers that enforce firm policies. Many deployments keep a human-in-the-loop for approvals and corrections so that models learn from verified outcomes. In the United States context, implementations commonly consider IRS recordkeeping rules and Generally Accepted Accounting Principles (GAAP) when structuring retention and classification. Security measures such as encryption and access controls are typically applied, and integrations are commonly performed through APIs or secure bank feeds.

- Intuit QuickBooks Online (QuickBooks Assistant) — Cloud accounting with embedded AI features for categorization and chat-based assistance. Typical small-business plan ranges may be about $20–$180 per month depending on features and user counts.

- Bill.com — Automated accounts payable and receivable workflows with invoice capture and approval routing commonly used by U.S. companies; pricing is often reported in the range of approximately $40–$120 per user per month for small and mid-market plans.

- BlackLine — Enterprise-focused automation for account reconciliations and close management used by many U.S. public and private companies; licensing and implementation costs often amount to several thousand U.S. dollars per year for enterprise deployments.

Comparing these examples shows differences in scale and focus: QuickBooks Online is typically positioned for small to mid-sized firms with embedded AI helpers for day-to-day bookkeeping; Bill.com focuses on AP/AR automation and workflow orchestration; BlackLine targets enterprise reconciliation and close processes. Selection and fit often depend on the size of the finance function, the complexity of accounting policies under U.S. GAAP, and existing system footprints. Organizations commonly evaluate integration effort, expected automation coverage, and the need for human review when assessing which approach aligns with their operations.

Data governance and auditability are frequent focal points during deployments. In the United States, finance teams often map automated classification outputs to established chart-of-accounts structures and maintain logs that support IRS compliance and audit trails. Models may be tuned to respect entity-level policies, cost-center allocations, and internal control frameworks. Where confidence thresholds are low, items are routed to an accountant for verification; where confidence is high, agents may post draft entries for batch review. This layered approach typically reduces manual cycles while preserving oversight.

Accuracy measurement and continuous improvement are operational considerations. Teams often track match rates for automated bank reconciliation, OCR extraction accuracy for invoices, and the percentage of transactions requiring manual recoding. Those metrics may be used to retrain models or refine rule sets. Integration testing with U.S. banking feeds, payroll systems, and tax reporting workflows is commonly scheduled before full production use. Vendors and internal teams often document rollback procedures and data backups to manage model errors and maintain financial statement integrity.

Cost and implementation complexity can vary substantially across the range of intelligent agents. Small businesses may deploy cloud tools within weeks, while enterprise reconciliations or ERP-integrated solutions often require months of configuration, testing, and change management. Typical cost drivers include user counts, volume of transactions, required connectors (bank, payroll, ERP), and the level of customization for internal controls. Contract terms often specify support levels and data handling responsibilities relevant to U.S. regulatory expectations.

In summary, intelligent finance agents automate classification, document capture, and reconciliation tasks by combining machine learning, rules, and human oversight in accounting workflows. Implementations in the United States typically consider GAAP alignment, IRS retention requirements, and system integration needs. Performance metrics, governance controls, and phased rollout approaches are commonly applied to manage risk and accuracy. The next sections examine practical components and considerations in more detail.