Home Equity Line Of Credit: How HELOCs Work And Key Features To Understand

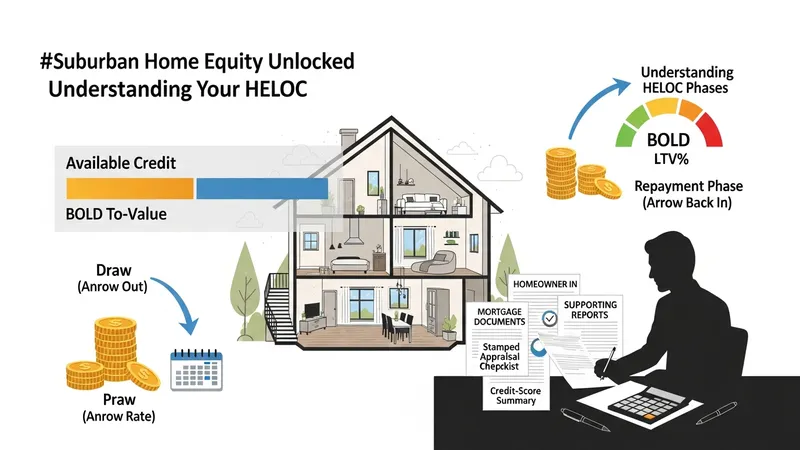

A home-secured revolving credit arrangement allows a homeowner to borrow against the portion of their residence they own, creating an ongoing access to funds up to an approved limit. Lenders typically set that limit by combining a homeowner’s existing mortgage balance with a maximum loan-to-value (LTV) ratio; the difference between that combined amount and the property’s assessed value becomes the available credit. Access to funds most often occurs during an initial “draw” period, followed by a repayment phase. Interest is frequently variable, tied to a published index plus a lender margin, and periodic payments may include interest only, principal and interest, or a blend over time.

Structurally, these lines of credit can include additional features such as conversion of outstanding balances to fixed-rate installments, seasonal or annual fees, and limits on how funds are used or accessed. Underwriting generally involves verification of income, credit history, and a property valuation. Costs and terms may vary by lender and market conditions; fees commonly associated with establishing this type of credit can sometimes be similar to those for other secured borrowing. The arrangement may also affect a homeowner’s overall debt profile and any subsequent borrowing.

- Variable-rate revolving line: A typical product where available credit can be drawn as needed and the interest rate changes with a market index, often featuring a defined draw period and later repayment phase.

- Fixed-rate conversion option: A feature offered by some lenders that allows borrowers to convert part or all of an outstanding balance to a fixed-rate installment, which may create a predictable repayment schedule for that portion.

- Amortizing hybrid: A structure that may start with an interest-only draw period then transition into scheduled principal-and-interest payments, blending short-term flexibility with longer-term amortization.

Comparative context helps clarify these examples: a variable-rate revolving line emphasizes flexibility during the draw period, while a fixed-rate conversion can reduce rate variability for selected balances. The hybrid structure tries to balance initial affordability with eventual principal repayment. Each option can interact with borrower circumstances differently—credit history, current mortgage balance, and property valuation can influence which features are available and at what cost. When assessing these structures, it is useful to consider how payment amounts might change over time and how that change aligns with a household’s likely cash flow patterns.

Determination of the approved credit limit often depends on a valuation process and on methods lenders use to calculate combined LTV. Valuation may be based on an appraisal, automated valuation model, or other acceptable metrics. Lenders sometimes set maximum combined LTVs that reflect perceived risk; those limits can vary by lender and market. Borrowers may encounter conditions such as seasoning requirements (how long they have owned the property) or limits tied to subordinate liens. These elements together influence the practical availability of credit and the flexibility of the arrangement.

Draw periods and repayment structures shape payment timing and amount. During a draw period, borrowers commonly pay only interest on outstanding balances, which keeps monthly payments lower but does not reduce principal. After the draw period concludes, the product typically shifts to scheduled principal-and-interest payments, which can substantially increase required monthly payments. Some lenders permit partial conversions or refinements of payment terms to manage that shift. Those mechanics often determine whether the arrangement remains affordable across changing financial circumstances.

Fees, periodic charges, and interest-rate formulas comprise the cost side of the arrangement. Lenders may assess one-time origination fees, appraisal costs, or ongoing annual fees; some products also include minimum draw or inactivity fees. The interest rate commonly equals a reference index plus a margin, and some products implement rate caps on periodic or lifetime increases. These cost components can affect the effective borrowing cost and should be considered alongside the structure of payments and repayment timing when comparing different offerings.

In summary, a homeowner-accessible revolving credit secured by residential equity combines a credit limit based on property value and outstanding debt with a draw period and subsequent repayment phase; variations include variable-rate access, fixed-rate conversion options, and hybrid amortization structures. Each example involves trade-offs between flexibility, payment predictability, and cost components. The next sections examine practical components and considerations in more detail.