VA Loans: Understanding Benefits And Eligibility In Banking

VA loans are specialized mortgage products that are made available through private lenders but backed by the United States Department of Veterans Affairs (VA). Their primary aim is to support eligible military service members, veterans, and certain surviving spouses in purchasing homes, refinancing existing mortgages, or making home improvements. The program is designed to recognize military service and may provide lending terms that differ from conventional and FHA loans in several key ways. Understanding how these loans function within banking processes is important for anyone considering this financing route.

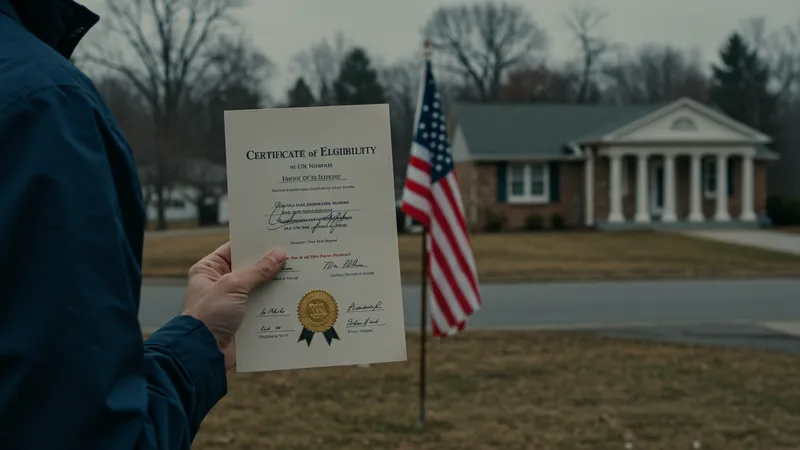

In banking, VA loans are processed in partnership with approved lenders while adhering to VA-specific requirements. The VA does not issue loans directly but guarantees a portion of the mortgage, which can reduce risk for lenders and may result in more flexible qualification standards for borrowers. Applicants typically must meet both service-related eligibility criteria and traditional credit or income guidelines, with documentation verified by both the lender and the VA to determine eligibility and benefit levels. A Certificate of Eligibility (COE) is a central document in this process.

- VA Purchase Loan: Provides funds to qualified borrowers for buying a primary residence with no down payment in many cases. Closing costs and funding fees may vary, with approximate fees ranging from 1.25% to 3.3% of the loan amount.

- VA Interest Rate Reduction Refinance Loan (IRRRL): Known as the streamlined refinance, this option typically allows borrowers with existing VA loans to seek a lower rate with limited income or appraisal requirements. Closing costs may be rolled into the new loan.

- VA Cash-Out Refinance Loan: Allows eligible homeowners to replace an existing mortgage with a new loan and access equity as cash for approved purposes such as debt consolidation or home renovations. Typical funding fees and closing costs can apply.

VA loans may offer unique advantages over other types of home financing. For example, borrowers can often secure a mortgage with little or no down payment, which can be significant for those with limited upfront savings. The VA guarantee also means that private mortgage insurance (PMI) is typically not required—another factor that can lessen the monthly costs compared to other loan types under similar credit circumstances.

Eligibility requirements for VA loans depend on military service or qualifying surviving spouse status, as well as discharge conditions, length of service, or deployment timeframes. The lending standards in banking for VA loans maintain typical credit assessments but often consider a wider range of income types, including military allowances and retirement benefits. Applicants are encouraged to verify their COE to determine eligibility before approaching banks or mortgage lenders.

A notable attribute is the VA funding fee, which helps sustain the program and may vary based on service type, loan amount, and down payment. This fee can generally be financed into the loan amount. While closing costs apply, the VA limits what borrowers may be charged, and some costs may even be paid by the seller, further reducing the initial expense for the eligible borrower.

Repayment structures for VA loans are generally similar to those for conventional fixed-rate or adjustable-rate mortgages. However, some banks may offer additional support or counseling resources for veteran borrowers, a reflection of the VA loan program’s focus on sustainable homeownership and the financial well-being of its participants. It is important to review the loan’s full terms and to consult the latest official VA sources as lending guidelines and benefit tables can change.

To summarize, VA loans in the U.S. banking context represent a specialized form of mortgage financing administered through both government and private banking channels. The next sections examine practical components and considerations in more detail.