Term Life Insurance: Key Features And How Coverage Works

Additional Features and Policy Considerations in Canadian Term Life Insurance

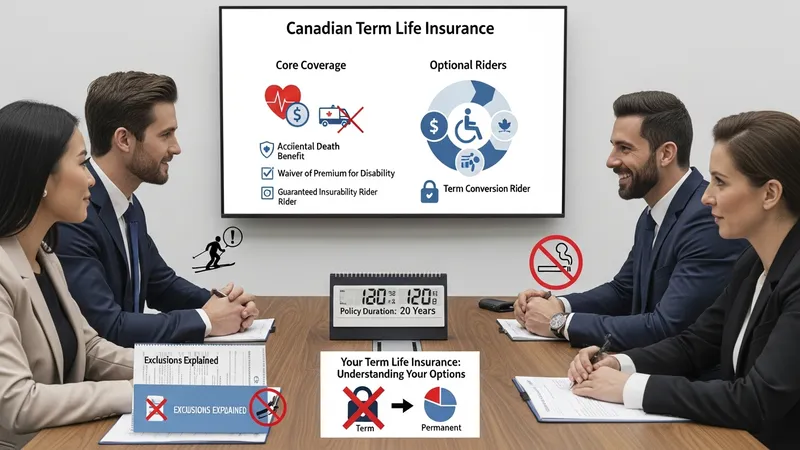

Many term life insurance policies in Canada incorporate optional riders or endorsements that can further tailor coverage to specific needs. Common features include accidental death benefits, waiver of premium for disability, and child protection riders. These optional features may increase premium costs but can provide extra financial support in designated scenarios.

Policy exclusions are explicitly stated in the policy contract. Standard exclusions may include non-payment of premiums, misstatement of age, or death due to certain activities identified at policy inception. Understanding these exclusions can prevent future misunderstandings and ensure beneficiaries are fully aware of claim eligibility criteria.

Canadian insurers are required to provide clear disclosures regarding cooling-off periods, allowing policyholders to review and cancel policies within a specified window (usually 10–30 days) for a full refund of premiums. This regulatory safeguard enables individuals to verify that the policy terms align with their expectations before full commitment.

As Canadian life insurance markets evolve, digital enrollment and online policy management tools have become increasingly accessible, offering policyholders new ways to track coverage, update information, or download documents. This trend may enhance transparency and consumer engagement within the term life insurance segment.