Term Life Insurance: Key Features And How Coverage Works

Policy Durations and Renewal Options in Term Life Insurance

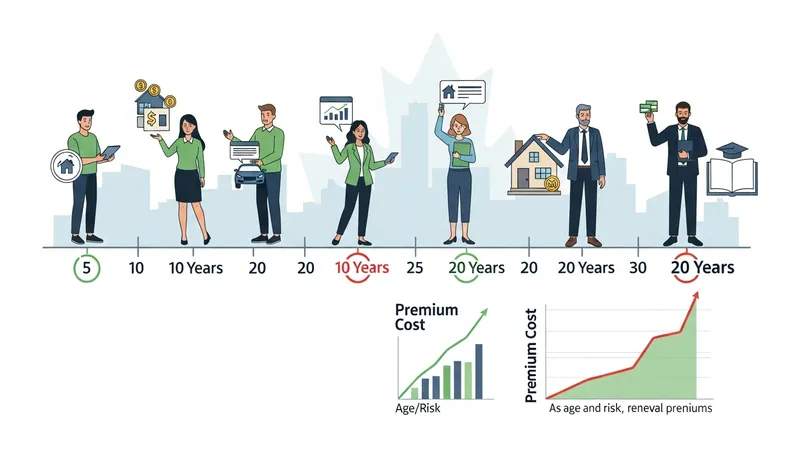

The durations available for term life insurance policies in Canada generally range from 5 to 30 years, with 10-year and 20-year terms among the most frequently selected. The chosen term aligns policy coverage with an individual’s specific time-bound financial commitments. Shorter terms may be considered by those with near-term obligations, while longer durations can be suited for families with young dependents or extended debts.

Renewal provisions allow policyholders to maintain coverage after the original period ends, typically through guaranteed renewal clauses. While renewal does not require new evidence of insurability, premiums often increase with each renewal based on the policyholder’s age bracket as set by the provider. This incremental pricing structure reflects statistical risk adjustments associated with advancing age.

Some Canadian insurers may also offer the ability to convert term coverage into permanent life insurance before a specified age or within a set timeframe, again without new medical assessments. Conversion can facilitate continuous insurance protection for those whose long-term insurance needs become apparent after the initial policy purchase.

It is important to note that not all term life insurance policies in Canada automatically renew; some may require explicit action from policyholders to continue coverage, while others cease at the end of the stated term. Policyholders are encouraged to review contract terms and renewal conditions when initiating or updating coverage.