Small Business Liability Insurance: Key Coverage Types And Provider Options Explained

Provider types and policy delivery considerations in the United States

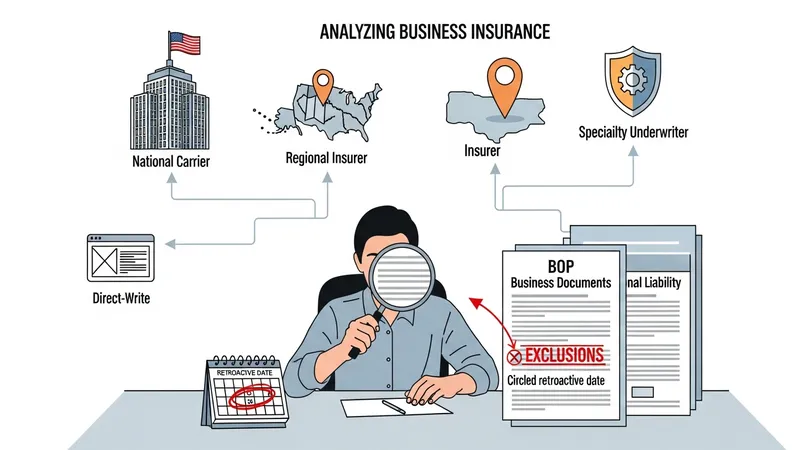

Small businesses in the United States encounter several provider types: national carriers that underwrite standard commercial forms, regional insurers that may specialize in local markets, and specialty underwriters that focus on niche industries or higher-risk operations. Some providers offer packaged products such as Business Owners Policies that combine liability and property coverages, while others issue standalone policies for particular exposures. Distribution channels include direct-write insurers, independent agents, and brokerage firms; selection of a delivery channel can affect policy forms, service options, and available endorsements.

Policy forms and insurer practices differ and should be reviewed carefully. Insurer forms may include proprietary wording or industry-standard language; small businesses can expect variations in exclusions, definitions, and claims-handling procedures. For example, professional liability policies from different underwriters may vary in how they define “professional services” or in available retroactive date options. Understanding these differences can influence how effectively a policy responds to specific incidents and how claims are administered after a report is made.

Service elements such as claims response time, local adjuster availability, and loss-control resources can affect the practical value of a policy. In the United States, larger carriers may offer broader national networks of adjusters and digital claims reporting, while regional carriers may provide more tailored local market expertise. Small businesses often assess whether a carrier’s claims handling aligns with their operational needs and whether the insurer provides access to risk-control resources that can help reduce future exposures.

Contractual relations with vendors, clients, and landlords frequently shape insurer selection and policy amendments. Many U.S. contracts require additional insured endorsements, waiver of subrogation, or specified limits; insurers differ in their willingness to provide certain endorsements and in the precise wording they will accept. Firms that work under government contracts or in regulated sectors should verify that proposed policy terms meet contract specifications and regulatory expectations as a practical measure rather than as a guarantee of coverage in every circumstance.