Senior Car Insurance: Key Factors That Influence Coverage Choices

Comparing and Reviewing Senior Car Insurance in Australia

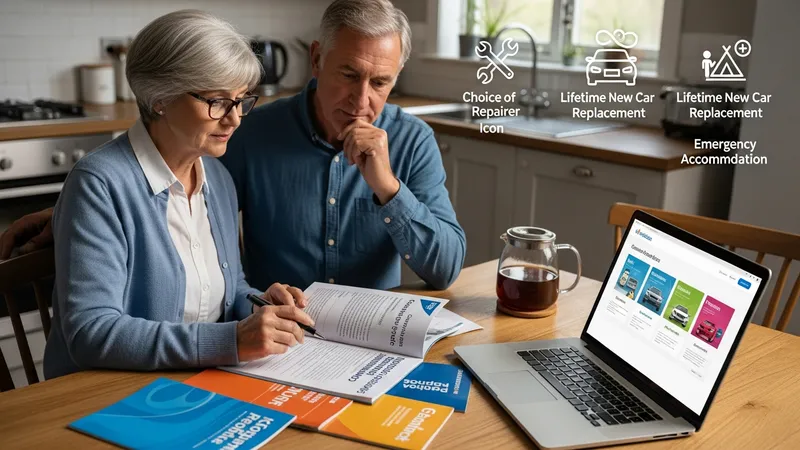

When comparing car insurance products, seniors in Australia may take several factors into account beyond just premium pricing. Particular attention is paid to the scope of coverage, including benefits such as choice of repairer, lifetime new car replacement, and emergency accommodation or transport. Annual policy costs can differ depending on included add-ons, declared vehicle use, and risk rating systems applied by the insurer.

Excess levels influence both upfront costs and post-claim expenses. Higher excesses may reduce annual premiums, but seniors need to consider outlay at claim time. The suitability of an excess level can depend on the policyholder’s financial position, frequency of claim history, and perceived risk tolerance. Some insurers may offer flexible excess options or waive excess under specific conditions, noted clearly in the PDS.

Customer service factors, such as claims processing speed, availability of helplines, and online management portals, commonly influence policyholder satisfaction. Australian seniors may value accessible communication options and clear support documentation, especially if managing policies for multiple vehicles or updating personal details.

It is typical for seniors to periodically review their car insurance agreements as circumstances change, including adjustments in driving habits, acquisition of new vehicles, or shifts in family arrangements. Many industry observers note a trend towards bundled home and car insurance due to the convenience and potential for streamlined administration, though price savings are not always guaranteed. Regular assessment enables alignment between personal needs and current cover options.