Private Lending For Property: Key Features, Loan Structures, And Typical Uses

Private Lending for Property: Cost Components and Exit Strategies

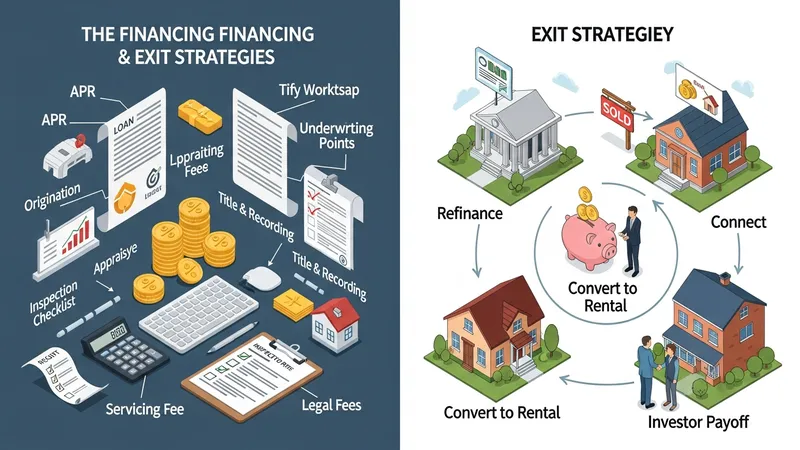

Cost components for private property loans in the United States commonly include interest, origination points, underwriting fees, appraisal and inspection costs, title and recording fees, and legal expenses. Interest may be stated as an annual percentage rate (APR) or a stated contract rate; additional fees and points can materially affect the loan’s effective cost. Some private lenders also charge servicing fees for handling ongoing collections. Borrowers typically factor these components into project budgets or acquisition analyses to assess whether the financing solution aligns with projected returns.

Exit strategies are central to private loan underwriting and pricing. Typical exits include selling the property, refinancing into a conventional mortgage, converting the property to a rental and paying down the loan with cash flow, or payoff through another investor arrangement. The plausibility and timing of the exit strategy influence acceptable term length, allowable LTV, and contingency reserves. Lenders in the United States often require evidence of the exit plan and may condition funding on milestones that support that plan.

Refinancing into conventional bank financing is a common exit for longer-term holds; however, transfer from private to conventional financing may require meeting conventional underwriting standards such as documented income or longer seasoning periods. For renovation projects, lenders often require substantial completion evidence before permitting conversion to a long-term loan. Tax and accounting implications for interest expense, capital improvements, and debt structuring are relevant in the U.S. context and are typically reviewed as part of project planning.

When evaluating private financing options, parties often weigh the total expected financing cost against timing flexibility and project needs. Private lending can provide speed and structural flexibility that may not be available from traditional lenders, but it can also carry higher explicit costs and different risk allocations. Careful documentation, realistic budgeting for fees and contingencies, and transparent exit planning help align expectations for both borrowers and non-bank lenders in U.S. property transactions.