Pet Insurance: Evaluating Policy Exclusions, Waiting Periods, And Restrictions In 2026

Waiting periods: timing structures and implications for claims

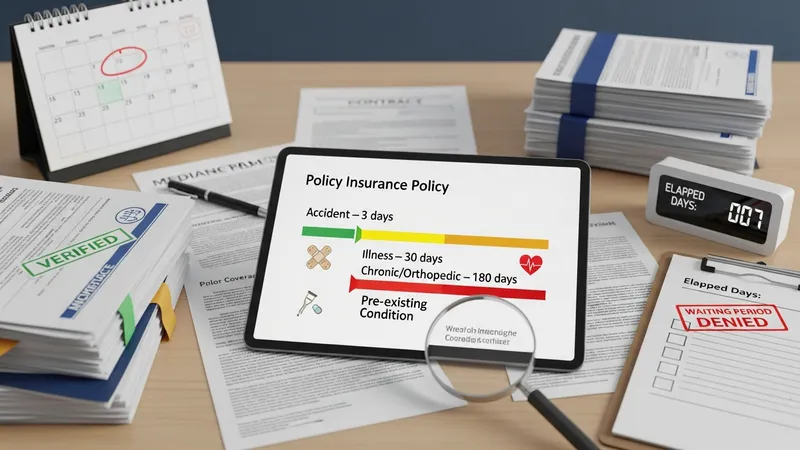

Waiting periods are contractual intervals that begin on policy inception and delay coverage for defined categories. Accident waiting periods are often shorter — in some plans a matter of days — while illness waiting periods often extend to multiple weeks. Certain chronic or orthopedic conditions can have longer waiting periods or condition-specific waiting rules. The presence and length of these periods can affect whether an early diagnosis will be covered, and policies may clearly state start and end dates for each category or rider within the plan.

Interaction with pre-existing condition rules is a common complexity: if a sign or symptom appears during a waiting period, insurers may classify it as pre-existing depending on definitions and documentation. Some policies may allow proof of prior health checks or continuous prior coverage to reduce or waive waiting periods under specific circumstances; others maintain strict waiting windows regardless of prior history. Understanding the required documentation and how insurers verify timing can clarify likely claim treatments.

Riders and add-ons may carry separate waiting periods from the base policy. For example, an optional wellness rider for vaccinations and preventive care may start coverage sooner or later than accident-and-illness benefits. This structure means that buying combined coverages does not necessarily synchronize activation dates. Policies may also offer reduced waiting periods in exchange for underwriting steps such as pre-enrollment exams, where available in the jurisdiction.

Seasonal or situational factors sometimes influence waiting-period planning: pets undergoing elective procedures soon after enrollment are frequently excluded until the waiting period lapses, which may affect timing of non-urgent surgeries. When comparing options, owners often note the relative lengths for accident versus illness coverage and any condition-specific waits, since those intervals can change the practical value of the policy during the initial months after purchase.