Mortgage & Real Estate Financing: Key Loan Types And How They Work

Documentation, Costs, and Ongoing Management related to Mortgage & Real Estate Financing: Key Loan Types and How They Work

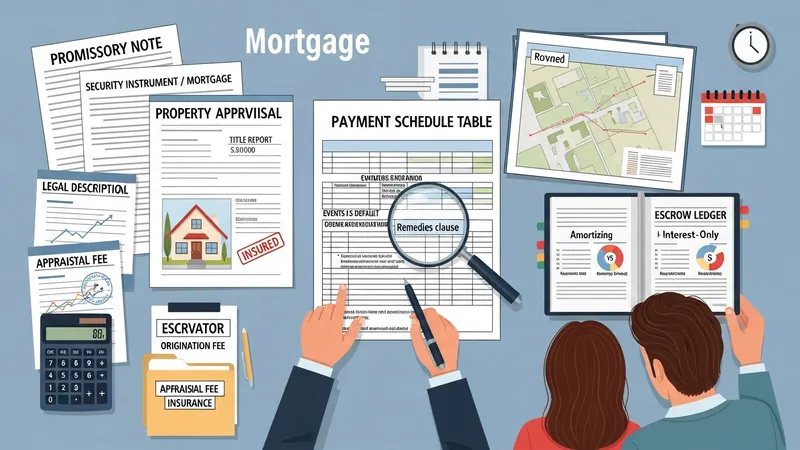

Documentation for property finance commonly includes a promissory note, security instrument or mortgage, disclosure statements, and agreement schedules that define payment terms, covenants, and events of default. Appraisals or valuations and title reports are standard attachments. Legal descriptions and insured title are necessary to secure the lender’s interest. The precise documentation package varies by jurisdiction and loan type, but clarity on rights and remedies in the loan documents is central to enforceability and operational management throughout the loan life.

Upfront and recurring costs can influence the effective cost of a loan type. Origination fees, appraisal fees, legal expenses, and any guarantee or insurance premiums add to initial costs, while servicing fees, escrow for taxes and insurance, and ongoing covenant monitoring contribute to periodic costs. For amortizing versus interest-only loans, the timing of principal repayments alters cash-flow implications and should be factored into affordability assessments. These cost components can vary with market conditions and lender practices.

Ongoing management includes monitoring compliance with covenants, performing periodic valuations or inspections for certain secured loans, and administering escrow accounts where applicable. For variable-rate products, lenders and borrowers must track rate-reset dates and notification requirements. Servicers also handle collections, payment accounting, and reporting. Understanding these administrative duties is important because they affect borrower obligations and the operational burden tied to different loan types.

When loans mature or require refinancing, parties typically assess current market conditions, remaining term, and any prepayment provisions. Strategies for managing upcoming payments may include negotiating amendments, arranging successor financing, or structuring paydown plans; outcomes depend on documentation, market liquidity, and borrower circumstances. Keeping records, maintaining insurance and tax payments, and communicating with the lender are practical considerations that often influence the smooth administration and transition of secured real-estate financing over time.