Life Insurance: Key Features And How Policies Work

Categories and Features of Life Insurance in the United Kingdom

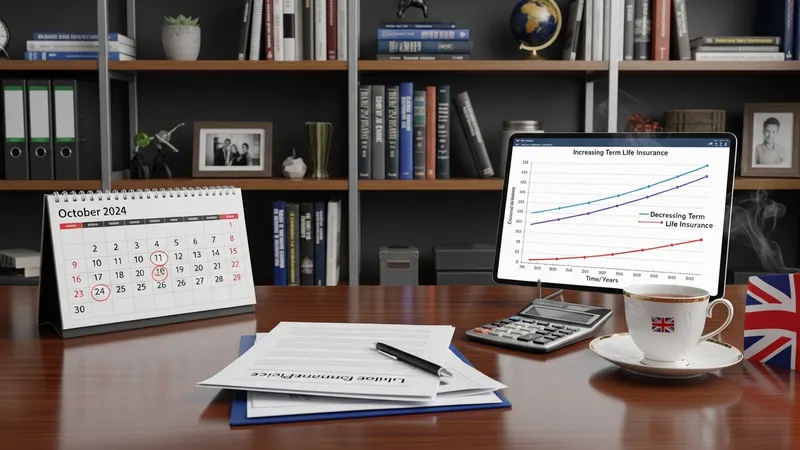

Life insurance in the United Kingdom can typically be grouped into several main categories. The two most prevalent formats are term life and whole-of-life policies. Term life insurance is often selected for its clear duration, providing coverage for a set number of years. In contrast, whole-of-life insurance offers ongoing protection that ends only on the policyholder’s death, as long as premiums continue to be paid. Other specialised forms may include decreasing term, which is often aligned with reducing mortgage balances, and family income benefit policies, which pay regular income instead of a lump sum. Options are designed to suit varied personal, financial, and estate planning objectives.

Each policy type may offer distinct features. Level term, for example, provides a fixed payout amount throughout the policy term, while increasing term allows the benefit and premium to rise with inflation. Whole-of-life policies may include an investment component, with certain products accumulating cash value, though such features are governed by strict regulations and not universally available. Add-ons, like critical illness cover, give extra flexibility but can impact total costs.

Legal and regulatory standards in the United Kingdom aim to ensure life insurance providers maintain transparency and fairness. The Financial Conduct Authority (FCA) supervises the sector, requiring all policies to include detailed terms, eligibility criteria, and an explanation of exclusions and limitations. This oversight is intended to help consumers evaluate the features and choose policies appropriate for their circumstances.

It is also common for providers to offer optional policy upgrades. Examples include index-linked benefits to maintain value over time and joint policies for couples. Each feature offered by UK insurers will set its own premiums and may be subject to eligibility or underwriting criteria. Such diversity allows consumers to select arrangements suited to changing life stages and financial plans.