Home Window Replacement Financing: Key Options For Managing Project Costs

Replacing home windows often requires structured payment arrangements that spread the project cost over time. Financing in this context refers to options homeowners may use to cover material and installation expenses, including loans, lines of credit, and vendor payment plans. These arrangements typically vary by interest rate, term length, required collateral, eligibility criteria, and how payments are scheduled. Understanding the basic concept helps separate the financial product (how funds are provided and repaid) from the project cost drivers (labor, materials, removal and disposal, and any permitting).

Key characteristics that distinguish financing choices include whether a product is secured or unsecured, how interest and fees are applied, and whether the instrument affects home equity. Some options may require a credit check, while others can be arranged through a contractor with deferred payment terms or promotional rates for limited periods. Timing also matters: the structure chosen can influence monthly cash flow, total interest paid over time, and readiness to address unexpected repairs or warranty-related follow-ups.

- Personal installment loan — An unsecured loan from a bank, credit union, or online lender repaid in fixed monthly installments; rates and typical terms can vary considerably depending on credit and lender policies.

- Home equity loan or home equity line of credit (HELOC) — Secured credit using residential equity; HELOCs often provide a flexible draw period while home equity loans usually offer a fixed principal and fixed term.

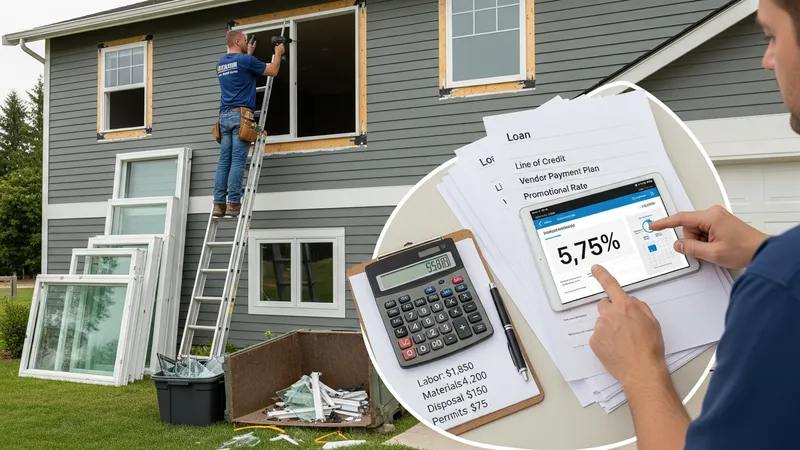

- Contractor or manufacturer financing — Payment plans offered directly by contractors or window manufacturers; these may include promotional periods, installment plans, or third-party point-of-sale financing arranged at the time of sale.

Comparing these examples, installment loans generally do not use the home as collateral and may close faster but can carry higher interest rates for borrowers with lower credit scores. Home equity products typically offer lower rates because they are secured by property value, yet they convert project cost into longer-term home-backed debt and may involve closing costs. Contractor or manufacturer financing may present convenience and bundled billing, and promotional rates can reduce short-term cost, though terms beyond promotions should be reviewed carefully.

Repayment structure is a core factor in cost management. Shorter loan terms often produce higher monthly payments but may reduce total interest paid, while longer terms lower monthly requirements at the expense of more interest over time. Some arrangements use variable interest rates, which may change payments, whereas fixed-rate options provide predictable monthly amounts. Borrowers may also encounter origination fees, prepayment penalties, or administrative charges; these items can change the effective cost and should be tracked when comparing offers.

Eligibility and credit considerations frequently influence which options are available. Lenders and financing programs typically assess credit score, income stability, existing debt levels, and sometimes property value when deciding terms. For secured products, loan-to-value (LTV) ratios can affect approval and pricing. Contractor-based plans may accept a broader range of credit profiles but could impose higher interest after promotional periods. Homeowners may often find that small balance projects behave differently in financing markets compared with larger remodeling loans.

Cost components of a window replacement project affect financing needs. Material quality, window type and energy performance, labor complexity, removal of old frames, and permitting can all increase the financing amount requested. Warranties and maintenance expectations can also influence decisions about loan length and whether to reserve contingency funds. Estimating realistic total project cost and including a cushion for unforeseen issues may reduce the need for later borrowing or costly short-term credit.

In summary, structured payment choices for window replacement combine product features, eligibility rules, and project cost drivers into a decision space that may affect monthly cash flow and total expenditures. Homeowners may typically benefit from comparing secured and unsecured options, understanding promotional fine print on vendor plans, and accounting for project-specific cost variables. The next sections examine practical components and considerations in more detail.