Hard Money Lenders: How Asset-Based Financing Works For Real Estate Investors

Financial metrics, valuation, and common underwriting benchmarks in U.S. markets

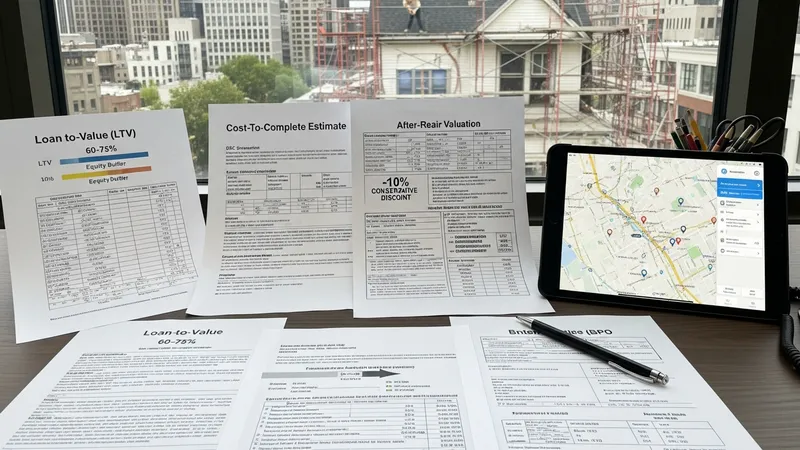

Key financial metrics used by lenders include loan-to-value (LTV), debt-service coverage when rental income is expected, and cost-to-complete estimates for renovation projects. In many U.S. markets, lenders may target LTVs that leave a reasonable equity buffer; common practice often results in maximum LTVs in the 60%–75% neighborhood depending on location and property class. Debt-service coverage ratios are more typical for income-producing properties; bridge loans for fix-and-flip projects may rely more on accurate repair costs and projected resale price than on ongoing income.

Valuation approaches often combine recent comparable sales, current market listings, and forward-looking adjustments for planned improvements. For properties requiring renovation, underwriters usually review contractor bids and contingency allowances to estimate post-repair value (after-repair value, or ARV). Conservative valuation practices may apply discounts to ARV to account for market liquidity and execution risk. Appraisals can be ordered by lenders, or a broker price opinion used for speed; the choice can affect perceived accuracy and the lender’s comfort with underwriting.

Financial modeling by investors frequently includes sensitivity analyses that test variations in sale price, timeline, and financing costs. Because interest and fees can materially affect net returns on short-term projects, scenarios often project a range of outcomes under slower sale conditions or higher repair costs. In several U.S. metropolitan areas, volatility in resale timelines has been observed, so conservative stress-testing of assumptions is a commonly suggested practice when preparing pro forma analyses. Lenders may require borrower reserves to cover unexpected cost increases.

Tax and accounting treatment for short-term asset-backed loans varies with the borrower’s enterprise structure and with lender entity type. Interest income for lenders and interest expense for borrowing entities are typically reported under U.S. tax rules, and depreciation rules apply to property owners. Parties often consult tax professionals to align loan structuring with intended tax outcomes. In certain cases, converting a short-term financed project to a rental property can change capitalization and expense treatment, which is relevant to both investor planning and long-term asset management.