Debt Consolidation And Credit Repair: Understanding How Professional Services Work

Cost factors and typical timelines for consolidation and credit report remediation

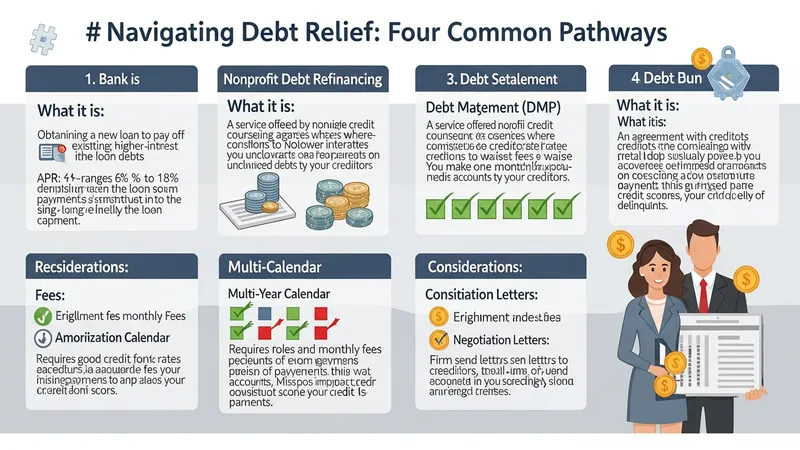

Costs associated with consolidation and credit-report services vary by provider type and method. A debt consolidation loan generally involves interest costs established at origination and may include origination or late fees; annual percentage rates (APRs) differ by lender and borrower credit profile. Debt management plans through nonprofit counselors may charge enrollment and monthly maintenance fees that are often disclosed up front, while debt settlement firms frequently charge fees tied to the total enrolled debt or amount saved through settlements. Credit report review services may bill a flat fee or monthly subscription for monitoring and dispute assistance.

Typical timelines also differ. Consolidation loans follow the loan’s amortization schedule, which may be two to seven years in common consumer scenarios depending on lender terms. DMPs often run multiple years until enrolled balances are satisfied through negotiated payments. Debt settlement processes may take several months to multiple years, depending on creditor responsiveness and the pace of accumulating settlement funds. Credit report dispute cycles initiated with bureaus commonly conclude in roughly 30 to 45 days for straightforward inquiries, though back-and-forth documentation can extend that period.

Potential indirect costs and considerations include the possible impact on credit scores and tax implications. Accounts included in a debt settlement may be reported as settled for less than the full balance and can lower a credit score in the short term; forgiven debt may trigger a Form 1099-C and potential taxable income reporting to the Internal Revenue Service in some circumstances. Consumers often weigh these downstream effects alongside immediate monthly payment relief and overall budget implications, recognizing that fiscal outcomes can vary by individual situation.

Insider considerations used by analysts and practitioners include scrutinizing fee disclosure documents, estimated timelines in written agreements, and whether a provider holds relevant registrations or memberships in nonprofit or industry organizations. Reviewing public complaint records—such as entries in the Consumer Financial Protection Bureau database—or verifying provider adherence to federal disclosure requirements may inform expectations about costs and timing. These considerations typically guide a measured evaluation rather than a prescriptive recommendation.