Auto Insurance For Seniors: Key Coverage Options And Considerations In 2026

Pricing factors, discounts, and usage-based options

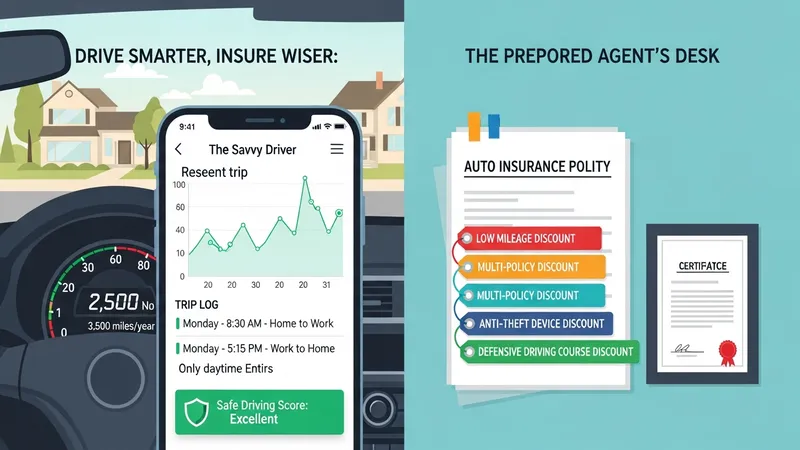

Premiums reflect multiple variables beyond chronological age, including driving history, vehicle type, annual mileage, and local claim patterns. Usage-based models that record mileage and driving behavior can adjust premium estimates to align with actual exposure. For example, drivers who restrict travel to daytime, avoid high-speed commuting, or drive fewer miles annually may see different pricing outcomes in programs that capture those patterns. Many insurers offer familiar discount categories—safe driving records, multi-policy bundling, anti-theft devices—but availability and criteria vary by provider and jurisdiction.

Discounts commonly referenced by insurers may include reductions for defensive driving courses, low annual mileage, or having certain safety features installed. Defensive driving or driver refresher courses sometimes influence underwriting in some markets, though their effect on premiums can be limited and typically depends on the insurer’s policy. Low-mileage discounts may apply where mileage is certified or tracked. It is important to view discounts as potential modifiers rather than guarantees; eligibility criteria and the magnitude of any premium change often differ among carriers.

Telematics-based programs may use mobile apps or installed devices to monitor driving patterns such as speed, braking, and time of day. These programs often provide periodic feedback and may lead to premium adjustments based on observed behavior. Data privacy and retention policies for telematics programs are relevant considerations: consumers typically see disclosures about what is collected and how long it is stored. For individuals who drive very little, pay-per-mile or mileage-banded pricing formats can sometimes produce a closer match between premium and actual exposure than flat-rate models.

Regional factors and market competition influence typical pricing trends. In areas with higher claim frequency or repair costs, premiums may be higher regardless of individual factors. Vehicle choice also plays a role: compact, lower-cost vehicles with strong safety ratings often carry different premiums than large or luxury vehicles. Where available, comparing how specific features and discounts apply to a given situation may clarify expected premium outcomes, while recognizing that final pricing results from each insurer’s underwriting methodology.